Key points

- Complexity of tax may lead to similar situations having different outcomes.

- Importance of electing to backdate a gift aid donation at the right time.

- Cliff edges can produce surprising results.

- Contrasting outcomes in Mayes and Lobler.

When a member of the public falls foul of a failed tax avoidance scheme, critics often express their lack of sympathy with the remark that the scheme’s advertised outcome was too good to be true. While I agree that non-tax experts should express a healthy scepticism when being sold a scheme, the criticism overlooks the fact that tax avoidance schemes are typically backed up by opinions from counsel and other tax experts.

In those circumstances, are non-tax experts entitled to believe the advice given, even if the tax outcome is very favourable when compared with the commercial realities? In general, and without wanting to condone the schemes, I would say that this is indeed the case.

The point has already arisen in the context of a First-tier Tribunal decision, which was considering whether the taxpayer had been negligent (the statutory forerunner of carelessness) when including a tax-favourable outcome on his tax return even though that outcome did not match the commercial realities. In Bayliss (TC5251), Judge Falk (now Mrs Justice Falk) and Member Michael Bell remarked:

‘Faced with their assurances that the scheme was legal and based on a tax “anomaly” we do not think that the fact that the terms of the loan were uncommercial, or that the contract for difference transaction itself was clearly uncommercial, demonstrate negligence for TMA 1970, s 95(1) purposes. We also do not think that the appellant was negligent for s 95(1) purposes in failing to obtain independent financial advice. If he had that might well have reinforced the rather obvious point that the entire transaction was uncommercial (which we think was clear enough to the appellant in any event), but would not have informed the appellant about how to fill in his tax return.’

Underlying the tribunal’s conclusions are a number of issues, which I do not believe should be controversial.

Tax is complex

First, I make the obvious point with no sense of satisfaction. Tax is complex and complexity gives rise to anomalies. Anomalies mean that what are ostensibly two similar situations can give rise to very different outcomes. Such differences will often look to be too good to be true.

To give some examples, I will start by considering VAT. Because that is a transactional tax, one might have thought that cliff-edges would be few and far between. But the categorisation of supplies provides its own artificial boundaries.

For example, is there really any significant difference between a chocolate hobnob and a jaffa cake? Even if there is, I can certainly see no justification for strawberry flavoured Nesquik to be subject to a different VAT rate from the chocolate flavoured variety.

Further, Neil Warren’s recent article ‘Summer treats’ (Taxation, 23 July 2020, page 12) highlighted that a packet of crisps sold by a takeaway establishment – a transaction that might have historically been subject to less VAT – still attracts a 20% rate, whereas crisps sold for on-site consumption are now subject to a 5% tax rate.

For consumers, the difference in VAT rates in these cases will rarely be significant. But, for the businesses operating in these fields, the potential for tax savings could appear to be too good to be true.

Cliff edges

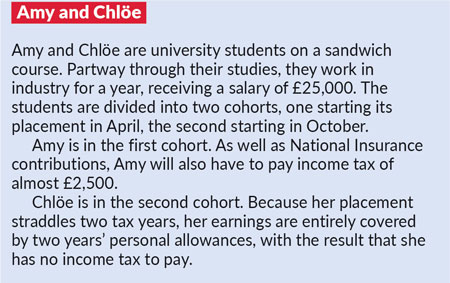

Second, particularly in the sphere of direct tax, the annual nature of the main taxes gives rise to its own set of anomalies. See Amy and Chlöe.

This is a classic case of two people doing identical work for the same salary, yet being subject to vastly different tax liabilities.

There are many good reasons for income tax to be considered by reference to an artificial period and such outcomes are inevitable. However, the point is that merely by putting herself into the second cohort, Chlöe has saved herself £2,500 (10% of her salary). Surely that is too good to be true.

For another example, I refer readers to a recent ‘Readers’ forum’ query (‘SDLT on main residence and investment property’, query 19,592, Taxation, 30 July 2020, page 29). This concerned the acquisition of two residential properties, one to be used by the purchasers as their main residence and the other as an investment.

The impact of Covid-19 delayed the purchase of the main residence so that (contrary to the initial plans) it would be the second property to be purchased. However, as the replies made clear, this had the unexpected outcome of allowing the couple to avoid the 3% surcharge on both purchases. That was a case where the couple had previously sold their earlier main residence and were living in rented accommodation. However, it highlights how a little foresight and timely professional advice can give rise to tax savings that would appear to many to be too good to be true.

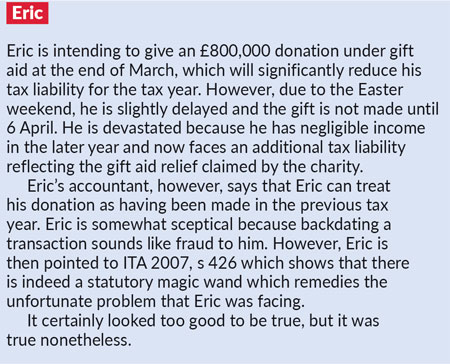

These examples might be explained as arising from design faults in the system. However, even so, they are design faults which can give rise to anomalously favourable outcomes. There are cases, though, where the tax system deliberately puts in a rule that, to the uninitiated, appears to be too good to be true. See Eric.

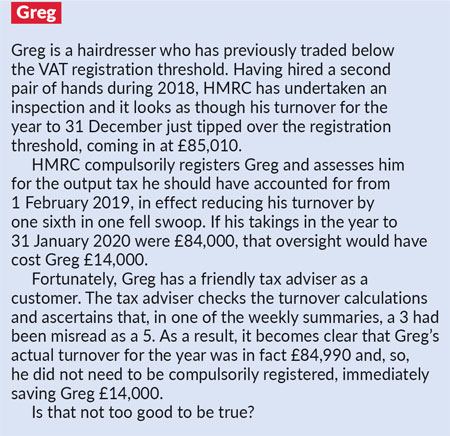

Even VAT has its own such cliff edges. See Greg.

Too bad to be true

However, to borrow from Isaac Newton, every tax reaction has its opposite. As well as cases where the outcome seems to be too good to be true, there are many where the outcome seems outrageously unfair.

Indeed, the contrast can be illustrated the contrasting cases of CRC v Mayes [2011] STC 1269 and Lobler v CRC [2015] STC 1893 where the complexities of the life insurance rules gave rise to, respectively, a very favourable and a disastrous tax outcome.

However, even in more prosaic areas, it is not difficult to find pitfalls lurking which can trip the unwary. The earlier examples provide potential illustrations.

In the case of Greg, but for the lucky discovery, Greg would have found himself £14,000 down simply for the sake of having earned £10 too much in the previous year. The effective marginal rate of 140,000% would shock most people.

However, I would like to focus on the example of Eric, the facts of which are loosely based on a recent case (Webster) heard by the High Court ([2020] EWHC 2275 (Ch)). However, unlike in Eric’s case, Mr Webster’s outcome risks being far too bad to be true. Mr Webster made a donation of £800,000 which he intended to carry back to the previous year. However, due to oversight, Mr Webster’s tax return reported the gift as having been for £400,000.

The earlier case of Cameron (TC415) held that such an entry on a tax return is incapable of being corrected – because ITA 2007, s 426 elections must be made on the original tax return and are not capable of being changed by way of a taxpayer amendment. On the basis of the Cameron case, one half of Mr Webster’s gift could be used to relieve the earlier year’s tax liability, albeit leaving the second half stranded in the later year, against which Mr Webster had no liability to relieve. So, Mr Webster would obtain tax relief in one year on £400,000, but owe the gift aid element on the second £400,000.

However, that is not the end of it. HMRC is taking a strict interpretation of s 426. It points out that the election applies to ‘the gift’ and not ‘a part of the gift’. As the gift was for £800,000, it is not possible to relate only £400,000 to the previous year. The department has, therefore, amended Mr Webster’s tax return so that none of the gift is treated as having been in the earlier year, leaving it all stranded in the later tax year. Thus, Mr Webster faces obtaining no tax relief at all and, further, must pay the income tax claimed by the charity. Surely that outcome is too bad to be true. Regrettably, subject to the First-tier Tribunal finding a charitable (no pun intended) reading of s 426, it is true.

Expect the unexpected

Tax does not always give logical or expected results, but that is not a licence for people to believe everything that anybody tells them. However, when a suitably qualified tax professional asserts that a particular outcome arises – whether good or bad – a lay taxpayer is entitled to believe them.

And if a critic ever suggests that professional advice should not have been followed simply because the advice was too good to be true, I would say that the critic is either being unfair or has a very poor understanding as to how tax actually works.