The new capital gains tax investors’ relief.

KEY POINTS

- A new capital gains tax relief for investment in qualifying shares.

- The relief provides for a reduced 10% tax rate.

- Although the relief is at the same rate as entrepreneurs’ relief, there are fundamental differences.

- Care will need to be taken on the activities of connected persons.

- Investors’ relief will be attractive for those who have exhausted their entitlement to entrepreneurs’ relief.

A new reduction from capital gains tax for gains on qualifying shares in a trading company, or a company that is the holding company of a trading group, is introduced by Finance (No 2) Bill 2016, cl 76. The new ‘investors’ relief’ can apply only to gains on shares subscribed for by the investor or their spouse or civil partner. The investor must not be an officer or employee of the company in question and neither can any person connected with him.

Although about 18 pages of the draft legislation (Sch 14) are needed to introduce this measure, the provision is relatively straightforward (see the PDF attached to the online version of this article here. The new legislation is inserted into TCGA 1992 and all references in this article are to that act unless specified otherwise. To set the scene, matters can be summarised as follows.

First, the core measures:

- Section 169VB – among other things, this determines whether the shares are qualifying and thus eligible for the new relief.

- Section 169VC – sets out the new relief. This is given in the form of a reduced 10% rate of capital gains tax that is separate from the already established 10% entrepreneurs’ relief rate.

- Section 169VH – caps the gains that can attract the 10% rate at £10m.

- Section 169VP – defines the term ‘subscribes for’ and addresses the impact of inter-spouse transfers.

- Section 169VQ – defines ‘trading company’ and ‘the holding company of a trading group’.

- Section 169VR – sets out general definitions.

Second, there are facilitating measures which comprise the following:

- Section 169VD to s 169VG – make provision to accommodate situations where it is necessary to identify particular shares; for example, where a shareholding is only partly comprised of qualifying shares.

- Section 169 VI to s 169VO – address the situation, after a company reorganisation of its share capital, where there is a share exchange or where there is a scheme of reconstruction. Section 169VO permits an election to disapply the s 127 paper-for-paper rule. In effect, this allows the taxpayer to opt to pay capital gains tax at 10% (instead of zero) should they have the foresight to recognise that the new shares acquired are not qualifying shares for the purposes of the new relief.

Third, there are counter-avoidance measures regarding return of value:

- A new Sch 7ZB introduces measures to disqualify otherwise qualifying shares if the investor (or an associate) receives value from the company during the period of restriction.

- The period of restriction begins one year before and ends on the third anniversary of the qualifying shares being issued.

- If the investor receives anything other than insignificant value (less than £1,001) during the period of restriction, the shares are to be treated as excluded shares.

- The above de minimis exclusion does not apply if, at any time from one year before the share issue to the end of the share issue date, arrangements exist to facilitate the return of value to a shareholder. In this case, any amount of value received is to be regarded as significant.

- Payments by the company such as interest representing no more than a reasonable commercial return on money lent to it, payments for the supply of goods not exceeding the market value thereof, and the payment of a dividend or other distribution not exceeding a normal return on any investment in shares or other securities, will not be regarded as payments giving rise to a return of value.

- Provisions exist to facilitate, in some circumstances, the making good to the company of any value received so as to avoid loss of relief.

In all, the counter-avoidance provisions are sensibly drawn and workable. Although each investor needs to be alert to the ‘return of value’ problem for the three years after each share issue, these measures are intended to counteract the sort of abuse that no reasonable investor would contemplate.

This rest of this article introduces practitioners to the core measure and leaves until another occasion commentary on the facilitating provisions – for example, the share identification rules required where a shareholding comprises ‘qualifying’ and ‘excluded’ shares – and a more detailed examination of the counter-avoidance provisions.

In a nutshell

Investors’ relief applies only to gains on the disposal of shares by an individual that can be shown to be ‘qualifying shares’, as defined by s 169VB, at ‘the relevant time’; that is, the time immediately before their disposal. If a capital gain arises on a disposal of one or more qualifying shares, the first £10m will be taxed at a new 10% rate – identical to that applicable under the entrepreneurs’ relief provisions.

A single investor can therefore enjoy £10m of gains taxed at the 10% entrepreneurs’ relief rate and £10m under the 10% investors’ relief rate. Although in his March Budget speech the chancellor referred to the extension of entrepreneurs’ relief in this regard, the legislative position is that investors’ relief is a new and quite separate and distinct measure.

A share is a ‘qualifying share at the relevant time’ if:

1. it can be shown to have been acquired by subscription by the taxpayer (as opposed to being purchased);

2. the taxpayer can demonstrate that he held the share continuously for the period beginning with the issue of the share and ending immediately before the disposal;

3. the share was issued on or after 17 March 2016;

4. when the share was issued, none of the shares or securities of the issuing company were listed on a recognised stock exchange (see below);

5. the share falls within the definition of an ‘ordinary share’ both at the time of its issue and at the time immediately before its disposal;

6. the issuing company:

- was a trading company or the holding company of a trading group (as defined by s 169VQ) when the share was issued; and

- has been so throughout the share-holding period;

1. the taxpayer can show that neither he nor a person connected with him has been an officer or employee of that company, or of a connected company, at any time in the share-holding period (see below in this regard); and

2. the period beginning with the date the share was issued and ending with the date of disposal is at least three years for shares issued on or after 6 April 2016 (and slightly longer for those issued between 17 March 2016 and

5 April 2016).

The share-holding period

To benefit from investors’ relief the taxpayer must demonstrate that the share-holding period is at least three years. However, in relation to shares issued between 17 March 2016 and 5 April 2016 this period is extended to include the time the shares were held before 6 April 2016. This is to accommodate the position of investors subscribing for shares between Budget day and the start of the 2016/17 tax year without enabling any claims to relief to be made on disposals before 2020/21. Simply, the minimum shareholding period for shares issued on or after 6 April 2016 is three years.

It should be noted that, although the counter-avoidance measures referred to above cease to apply after the third anniversary of the share issue, the core qualifying conditions continue throughout the entire period of ownership. Therefore, if an individual expecting to benefit from investors’ relief becomes an employee of the company while still holding the shares, his entitlement (based on the Bill as drafted) will cease and will not be capable of being resurrected.

Likewise, should a child of the investor become an employee of the company this too would terminate any possible entitlement to relief. This would also be the case if the investor marries an employee of the company while still owning the shares subscribed for. Should the shareholder divorce before they sell their otherwise qualifying shares in the employer company, they will have lost entitlement to relief as well as their spouse. It is to be hoped that there will be some movement in this area. The absurdity of the position as things stand is highlighted by the fact that the very similar relief available under the entrepreneurs’ relief legislation requires the shareholder to be either an officer or an employee.

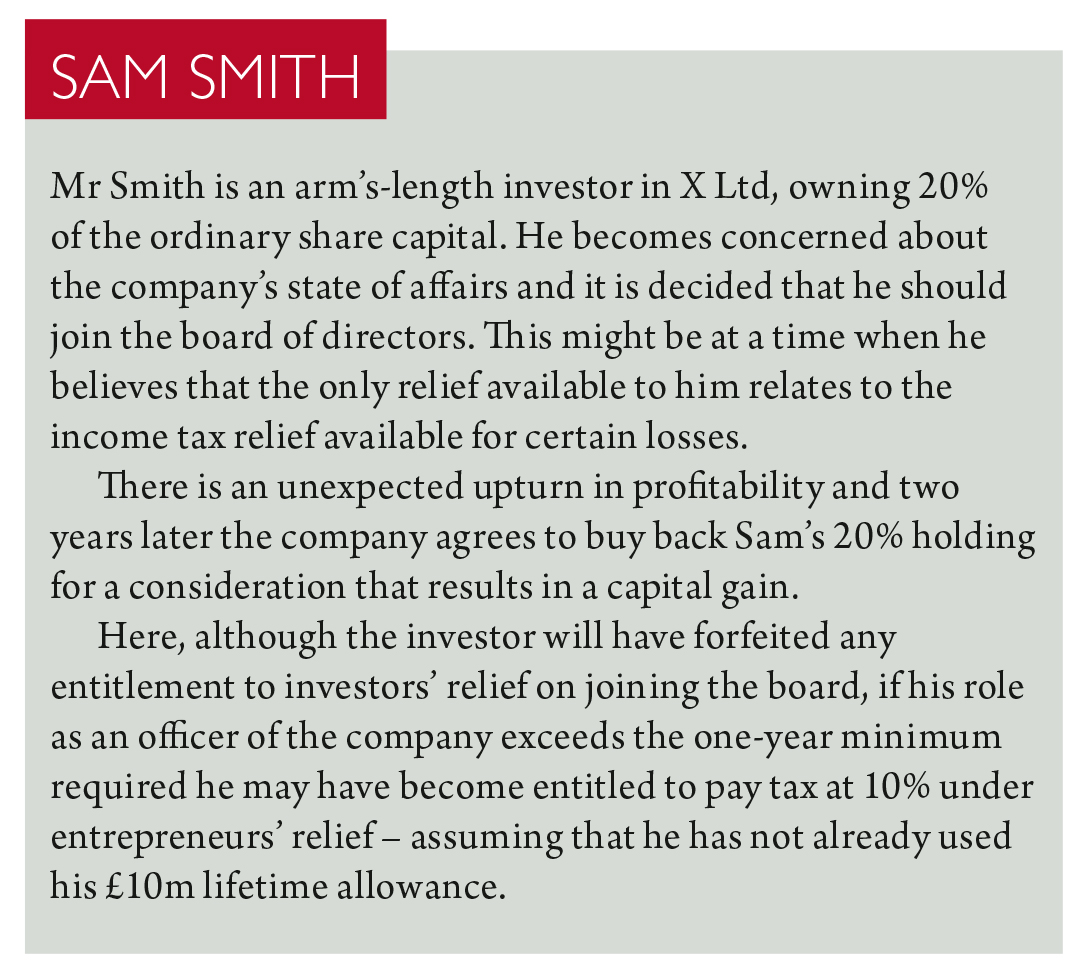

It is easy to imagine a situation such as that in Sam Smith.

‘Unlisted’ shares

An Inland Revenue press release of 20 February 1995 confirmed that shares and securities traded on the alternative investment market (AIM) will not be treated as ‘quoted’ or ‘listed’ for tax purposes. It is understood that this continues to be HMRC’s policy in connection with the interpretation of investors’ relief. Further, the advice in its Capital Gains Manual at CG50278 – which, among other things, states that ‘shares and securities traded on [AIM] are treated as neither listed nor quoted’ – is to apply for investors’ relief as well as the other relieving provisions.

Accordingly, shares acquired by subscription in a trading company, which at the time of issue had some of its shares traded on AIM, will normally satisfy the ‘unlisted’ requirement. However, readers should not overlook the possibility of a company whose shares are traded on AIM also having a ‘secondary listing’ elsewhere. If this is on an overseas a stock exchange recognised by HMRC the investors’ relief may be lost. Fortunately, the unlisted requirement in s 169VB(2)(d) need be satisfied only when the shares are subscribed for and a secondary listing after the taxpayer subscribed for his shares will not prejudice the relief. Contrast this with the position on inheritance tax business property relief highlighted in my 2014 article ‘Don’t quote me’ where relief can be lost overnight.

It appears to matter not that, after the issue date, the trading company obtains its first listing on a recognised exchange. This seems to be so even though there might be arrangements in place at the issue date for an initial public offering on the London Stock Exchange. However, see below if there is a tax avoidance motive to a share issue.

Trustees and jointly-held shares

As Finance (No 2) Bill stands, investors’ relief does not extend to shares subscribed for by trustees. Representations are no doubt being made to HMRC in this connection, but matters need careful attention. Given the exclusion of individual investors who are employees at the time of issue of the shares (or become so during the share-holding period), the matter of beneficiaries becoming employees will need to be addressed and it may be that the current exclusion of trust gains will continue. Consideration of this issue may result in the exclusion of officers or employees being dropped altogether. It is to be hoped that ministers will ask whether this exclusion achieves anything in terms of the policy objective.

Again, as the Bill is drafted, investors’ relief applies only to the sole holder of any qualifying share (s 169VC(6)). Thus, a husband and wife who invest jointly by subscribing for 10% of the shares in Y Ltd will not be entitled to the new relief – even though if each had subscribed for a 5% shareholding any gain could qualify. It is to be hoped that this unnecessary complication will be removed as the Bill progresses.

Share subscriptions

Section 169VP requires that the shares subscribed for must be:

1. fully paid up at the time of issue with the consideration paid to the company consisting wholly of cash; and

2. issued under a bargain at arm’s length.

Further, s 169VP requires that a qualifying share must be subscribed for, and issued, for genuine commercial reasons and not as part of a scheme or arrangement the main purpose or one of the main purposes of which was the avoidance of tax. It remains to be seen what impact the ‘commercial reason’ will have in practice.

The securing of a tax advantage in the form of the very investors’ relief that parliament will clearly intend (if the Bill is passed so as to become an Act) will not be regarded as tax avoidance. That said, it is possible to imagine contrived situations where shares are subscribed for and where arrangements are in place to guarantee one or more investors a capital gain on exit – for example, using a company buy-back route. However, the reality is that this test is best viewed as HMRC’s equivalent of an anti-embarrassment clause in a simple sale agreement. Neither party thinks they have overlooked any angle but, just in case, a clause is inserted that covers an eventuality that might need addressing in future.

Although not necessarily conclusive, the date on which shares are issued is likely to be the date upon which the share register of the company first reflects their existence. It is not necessarily the date of application. Indeed, it appears that shares issued on or after 17 March 2016, and which were applied for before Budget day, will have the potential to be qualifying shares.

Inter-spouse transfers

Section 169VP also contains a measure to protect relief when an individual (A) subscribed for shares – or is treated under this subsection as having subscribed for them – which are transferred to another individual (B) if A was living together with B as their spouse or civil partner at that time.

Here, B is to be treated as having subscribed for the shares and any period for which A held the shares is to be added to, and treated as part of, the period for which B held them, ending with a disposal to a third party.

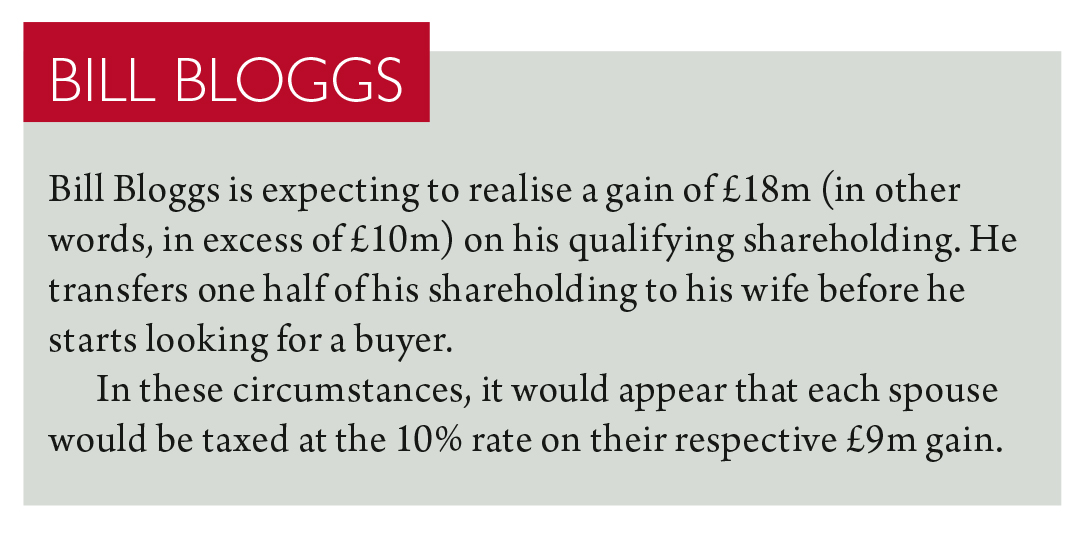

Accordingly, if the qualifying conditions continue to be met, any gain realised by B on a disposal to a third party may qualify for relief even if B’s actual ownership lasted less than three years. See Bill Bloggs.

Definitions

Section 169VQ states that the terms ‘trading company’ and ‘the holding company of a trading group’ have the same meaning as in s 165, and as defined in s 165A. It will be seen, therefore, that these definitions are not quite the same as those applying as regards entrepreneurs’ relief (which uses an amended form of s 165A). Readers may be familiar with these definitions, but the entrepreneurs’ relief differences can be found at s 169S(4A).

Section 169VR contains some important definitions for the purpose of the investor’s relief. For example, the term ‘ordinary shares’ is defined as meaning any shares forming part of the company’s ordinary share capital within the meaning given by ITA 2007, s 989. Accordingly, ‘ordinary share capital’ for this purpose means all the company’s issued share capital (however described), other than capital the holders of which have a right to a dividend at a fixed rate, but no other right to share in the company’s profits.

Section 169VB requires the investor to demonstrate that neither he nor a person connected with him has been an officer or employee of the company invested in (or of one connected with that company). This requirement must be satisfied throughout the entire share-holding period.

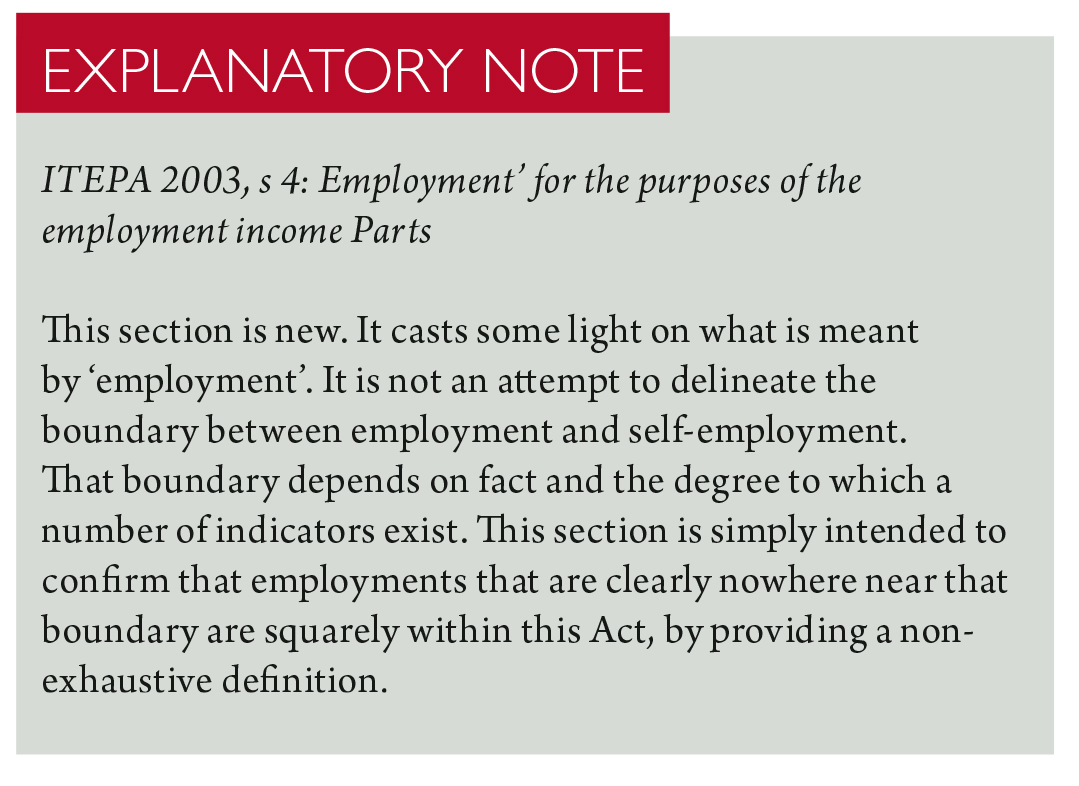

The terms ‘office’ and ‘employment’ have the meanings given by ITEPA 2003, s 5(3) and s 4 respectively. In particular, ‘office’ includes any position that has an existence independent of the person who holds it and may be filled by successive holders. This includes the position of a director and, assuming the company continues to have such a position, the role of company secretary.

ITEPA 2003, s 4 defines ‘employment’, including in particular:

1. any employment under a contract of service;

2. any employment under a contract of apprenticeship; and

3. any employment in the service of the Crown.

Section 4 goes on to state that the terms ‘employed’, ‘employee’ and ‘employer’ have corresponding meanings. It should be noted, however, that this is not an exhaustive definition – and may cause problems in some situations. The Treasury published an Explanatory Note on the interpretation of the then new ITEPA 2003, s 4.

Being a ‘non-exhaustive definition’, problems may arise if an individual who regularly attends the premises of a company invested in – and participates in meetings, carries out reviews of processes or generally keeps an eye on developments and suchlike – may be regarded by HMRC as an employee even though the investor is not being paid for his time. HMRC might take the view that the so-called ‘duck test’ applies: if something looks like a duck, walks like a duck and sounds like a duck, the overwhelming chances are that it is a duck.

Applying the duck test, if the conduct of the investor in attending the company’s premises regularly, meeting staff generally and attending board meetings etc and, possibly, carrying out simple tasks is difficult to distinguish from that of employees on the payroll, HMRC may seek to assert that the shareholder is in fact an employee, albeit unpaid. In this connection, it should be noted that the First-tier Tribunal inRichard Hirst v HMRC (TC04038), referring to the ITEPA 2003 definition, stated: ‘[The s 4] definition is inclusive rather than exhaustive.’ This supports the view that it extends to individuals who, although not paid as employees, are conducting themselves in a like manner. It is to be hoped that the legislation will be revised to contain an exhaustive definition of the term employee.

Connected person

Section 286 defines ‘connected person’ for all purposes of TCGA 1992 (unless modified). Shares held by individuals who are neither officers nor employees, but are connected with persons who are or become officers or employees of the company in which the taxpayer has invested (or in a company connected with it) at any time during the share-holding period, are excluded from the investors’ relief.

The primary rule is that a person is connected with an individual if that person is the individual’s: spouse or civil partner; relative; or the spouse or civil partner of a relative, of the individual or of the individual’s spouse or civil partner.

For this purpose ‘relative’ means brother, sister, ancestor or lineal descendant.

Conclusion

This new relief is to be welcomed as encouraging external investors to put their money at risk. Although there is a lot to think about in any given situation, the relief is far more straightforward than that applicable to, say, investors in enterprise investment schemes. Strangely, the Treasury has decided not to make any attempt to exclude heavily asset-backed trading companies such as those operating hotels or farming. Property development companies can also source capital highlighting the advantage offered by the investors’ relief provisions. This will be particularly attractive for individuals who have exhausted their lifetime entrepreneurs’ relief allowance or expect to do so when investments already made are realised.

Some amendments to these new provisions are to be expected as the Bill makes its way through parliament and readers should pay careful attention to the final wording of the provisions once royal assent has taken place.